The Iran crisis could not have come at a worse time for packaged food companies, which are still rebuilding volumes and margins from the pricing waves that have hit consumers hard. And, in some cases, hurt brand reputation too.

No one has a crystal ball to pinpoint how long the US-Israel-led war with Iran is likely to last but, as we near the end of a third week of conflict and the continued blockage of the key Strait of Hormuz oil shipping route, concern is building over the wider implications and risks – in the short- and longer-term. In the meantime, energy-linked inflation concerns are intensifying.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

It appears the world could be in for a longer haul than the four to five weeks President Trump had initially envisaged but the lack of support from major US allies in Europe could very well bring an end to the hostilities closer. Uncertainty is likely to ensue whatever the resolution to the war might be, particularly given Iran’s retaliatory attacks on its Middle East neighbours.

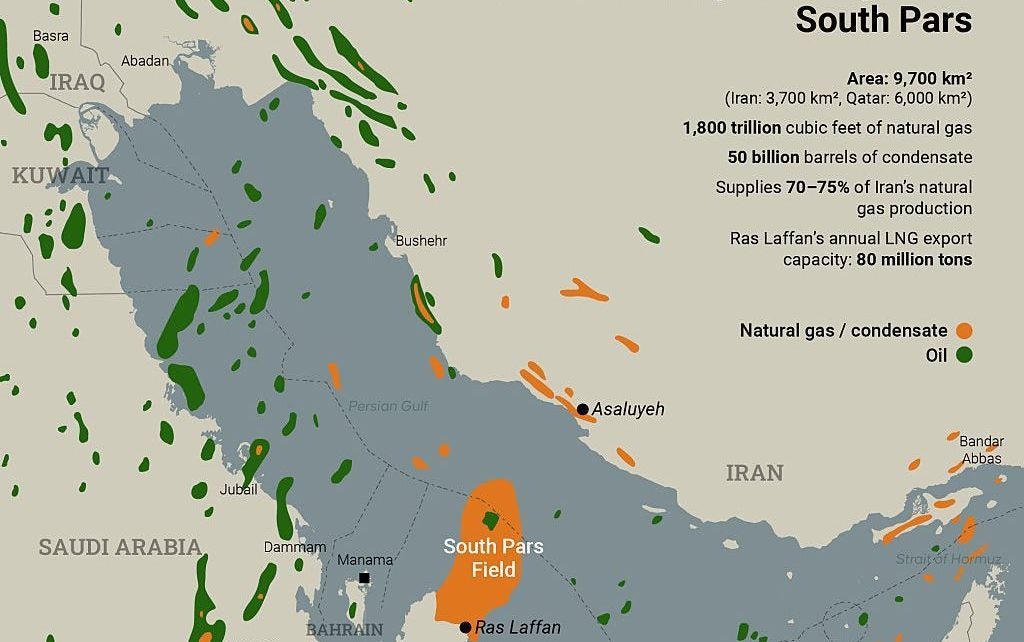

Those attacks, and the prospects of a drawn-out conflict, escalated this week when Israel bombed the South Pars gas field, the world’s largest, shared between Iran and Qatar. Brent crude spiked above $116 a barrel on Thursday (19 March) as Tehran launched a tit-for-tat response on Gulf oil refineries.

For food, the implications are perhaps less severe than when Russia invaded Ukraine in February 2022, at least for now.

Then, prices of major inputs exported from Ukraine such as wheat, sunflower oil and fertiliser spiked, compounding an inflationary trend across the supply chain that some manufacturers and global monetary policy makers are still grappling with today. And, of course, consumers had to stomach the burden, too, in many cases turning to lower-priced private label and discounters.

Fertiliser blow

Unlike Ukraine, the Middle East is a net food importer, which softens potential adverse impacts on exporters to the region somewhat, albeit alternative transport routes may have to be utilised.

However, the Middle East is a major supplier of fertiliser. According to Stefano Di Napoli, founder and director at consultancy Consumer Products Growth Strategy, it accounts for around 40% of the world’s supply.

If the war ends up being a protracted conflict, fertiliser stocks could be depleted, putting pressure on farmers and agricultural crops, raising the risk of higher prices of fresh goods on supermarket shelves. It is fortuitous the western world is entering spring, with the summer months around the corner.

In the short term, the major risk to the food industry is oil and gas – prices have already spiked and are likely to remain volatile while the conflict lasts. Energy-intensive sectors such as bakery and baked goods, bread and biscuits for instance, along with chilled and frozen categories, are likely to be more exposed than others, as they were when the Russia-Ukraine crisis kicked off.

Logistics, transportation and packaging costs could rise too, while for each day the conflict lasts the inflation candle burns brighter, with stagflation concerns emerging and central banks pausing in their interest-rate cutting cycle.

Di Napoli says increases in fertiliser prices from the Middle East will definitely raise agriculture costs if shipments are disrupted for any length of time, with the potential pass-through effect to shelf prices.

“Companies will not feel the pressure immediately. It will probably be six to nine months before agricultural costs have an impact. The longer the conflict goes on, that will be the bigger concern for food manufacturers.

“It’s not the same scale as Russia invading Ukraine but is still an important element on the cost side, especially if you think that consumers will feel the pressure from an inflationary point of view as well.”

Impact on agriculture

Andy Searle, a partner at consultancy AlixPartners, also suggests fertiliser is not an immediate risk for food but it would be over the medium to long term, potentially reigniting inflation along with all the knock-on effects.

Prices on-shelf will be shielded for now just because of where the western world currently is in the agricultural cycle as the spring equinox begins.

“It’s March – people have planted stuff, they’re growing stuff and pulling stuff out but, when it comes to buying fertilisers now and the global price is up, to get stuff that’s coming out of the ground in six months, that’s going to have a higher cost attached to it,” Searle says.

“If the conflict carries on for a little bit longer, even if it then goes away in a few months, that higher price of fertiliser is already in the ground. And farmers operate on pretty thin margins.”

You could quite easily see a scenario in which the impact we had in Ukraine comes again

Andy Searle, AlixPartners

The pressure on those margins could be exacerbated if the higher cost of oil and gas feed through to red diesel used in agriculture, while consumers and transportation companies face higher costs at the forecourt pumps in Europe. Ultimately, the pass-through will land on food manufacturers, he says.

“You could quite easily see a scenario in which the impact we had in Ukraine comes again – higher fuel prices, higher fertiliser prices, leading to higher crop prices, higher wage inflation and all of the cost lines on food businesses globally, but particularly across Europe, where we’re a net importer of gas, oil and fertilisers,” Searle argues.

Grain effect

As a globally traded commodity, grain prices are also vulnerable to higher costs for fertiliser, fuel and transportation, according to Paul Mohr, a managing director specialising in food and consumer goods at consultancy group Inverto. Wheat futures have already spiked to multi-month highs.

Those higher prices would eventually filter through to downstream products such as flour and bread, while dairy and meat would also be affected given grains are used in animal feed, Mohr says.

“The impact is therefore global but especially pronounced in regions that are highly dependent on imports or long supply chains.

“Over the past five to ten years, geopolitical disruptions such as Covid-19, the Ukraine war, the Red Sea crisis, and other geopolitical tensions have repeatedly demonstrated how quickly availability and costs of goods can shift,” he says.

“At present, the most immediate impact is on fuel costs, with varying expectations around how long and how severe the increase will be. Most companies are closely monitoring the situation and currently view it as somewhat temporary but preparedness remains essential.”

Richard Wyborn, a partner at consultancy Food Strategy Associates, says the cost of food packaging, especially plastics, is likely to increase, while energy-intensive food sectors like the processing of certain raw materials such as sugar and oils, along with bakery could be more exposed to higher costs.

“The inflation pressure that we saw when Russia invaded Ukraine, that occurred over a period of about six months, if we go into the winter and prices have risen sharply, then I think you’ll start to see discomfort,” Wyborn explains.

However, he adds: “It feels like people are prepared to do whatever it takes to keep a lid on inflation, a lid on energy prices, having seen how negative the impact can be on the economy, on individuals, on prospects – you saw a big release in terms of reserves of oil last week.

“Longer term, there’s greater recognition of the need to invest where possible in automation and in a drive for efficiency because the shocks have been so frequent that people really need to find ways to increase energy efficiency but also reduce labour costs to enable them to be a bit more resilient to these shocks.”

Scenario planning

Food manufacturers have not yet come out in droves to express concerns over the conflict and those that have voiced any opinion are of the assumption the war will be short-lived but with an element of ‘if’ over the longer-term risk.

Searle at AlixPartners says worry is perhaps too strong a word to reflect sentiment in boardrooms. It’s more, he suggests, a “heightened state of awareness”.

“I think broadly there’s a bigger understanding of their supply chains than there used to be, which allows them to hopefully at least understand the risks that are involved,” Searle adds. “There will be scenario planning around the length of the conflict, what that means going forward, and what that means for their P&Ls.”

Oil and gas prices are fluctuating around daily events in the Middle East but, with Brent flirting with $120 a barrel on Thursday and gas spiking 25% on the back of the South Pars attack, executives will surely be taking stock.

The inflationary impact cannot be ignored for too long – even the Bank of England upped its forecast on Thursday for 2026 after keeping rates on hold. And the strategy implications for food manufacturers rebuilding volumes and margins could be very disruptive.

AlixPartners puts together a so-called disruption index based on executive discussions across industries around the world. There were still levels of disquiet at the last call in January, particularly for consumer products.

Searle says the Middle East conflict is likely to amplify the fragile sentiment, agreeing with the hypothesis that frozen, chilled and baked goods might be more susceptible to energy shocks than other food categories.

Pricing challenge

In the event the crisis is prolonged, raising shelf prices will be a challenge, especially when consumer sentiment is already “pretty low”, Searle says.

“We’re in a market now where financial markets like the higher margins that everyone’s got and want to keep that when the pressure on everyone is to get back into volume growth rather than value growth,” he suggests.

“If it only carries on for another four or five weeks, I think people will take it as a hit and not pass it on. If it’s more structural, they’re going to have to do something again. But I’m not sure anyone’s going to want to be the leader in moving up prices.”

Companies need to recover volume and to recover these volumes they will not be able to pass on the cost

Stefano Di Napoli, Consumer Products Growth Strategy

Di Napoli suggests stock markets are already building the risks into their share wagers in packaged food companies as he predicts private label is likely to see a further uplift on any inflation pass-through to shelf prices.

“Companies need to recover volume and to recover these volumes they will not be able to pass on the cost,” Di Napoli argues. “I think they will be open to accepting a lower margin, which will have a negative effect on their stock prices and valuation.

“They have learned that these changes in pricing and putting pressure on consumers is negatively affecting their brand. And we know that for packaged foods, brand power is absolutely critical, especially with private label in European countries such as the UK, the Netherlands and Spain growing.”

Pricing mechanisms will largely depend on the direction of travel of inflation, which had come down significantly before the US-Israeli airstrikes on Iran began on 28 February. Oil and gas of course will be the main determinants.

Otherwise, food manufacturers will have their backs to the wall. After all, many are still yet to fully recover volumes and some are still pricing to offset the last bout of food inflation, which reached double digits in many countries.

“If we end up with sustained double-digit inflation, then companies will have no choice. They’ll have to increase prices to retailers or they’ll go to the wall. But we’re far from being there,” Wyborn says with optimism.

They do have other levers to pull, as well as the pricing option, as Mohr suggests, such as “adjusting packaging or product sizes, pursuing premiumisation strategies, and optimising channel mix to protect margins while maintaining competitiveness”.

It all sounds very familiar, mirroring the counter-inflationary strategies employed by food producers over the past four or five years. And consumers are still feeling the pinch now. Hopes will rest on a short-lived conflict.

“A short-term increase may be absorbed to protect demand, whereas a prolonged or significant rise would make cost pass-through more likely,” Mohr says.

“In the short term, many manufacturers are likely to see pressure on profits, as countermeasures such as pricing adjustments or cost optimisation typically take time to take effect.”