Global olive oil prices have surged in recent times following weak harvests from the chief production regions.

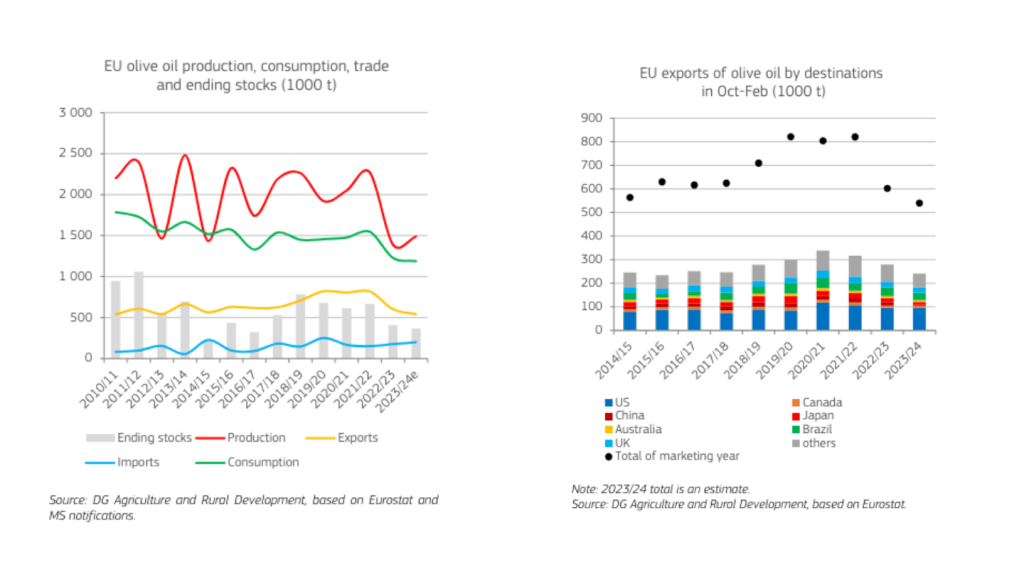

Total EU olive oil production is estimated by the European Commission to reach 1.49 million metric tonnes in the 2023/24 season, marking a 7% jump on the season before, according to a recent report.

Go deeper with GlobalData

Discover B2B Marketing That Performs

Combine business intelligence and editorial excellence to reach engaged professionals across 36 leading media platforms.

However, this number stands 28% below the five-year average and carryover into the new season, particularly in Spain, is down at circa 200,000 metric tonnes, compared to the usual figure of around 500,000 metric tonnes, showing a hangover from poor yields in the prior season.

Spain, which produces circa 50% of the world’s olive oil, has suffered the most in its production, off the back of droughts and inflation in the last 18 months.

Jaén in Spain is one of the “most representative olive oil markets of the EU”, according to the International Olive Oil Council (IOC), covering more than 60% of global olive oil production.

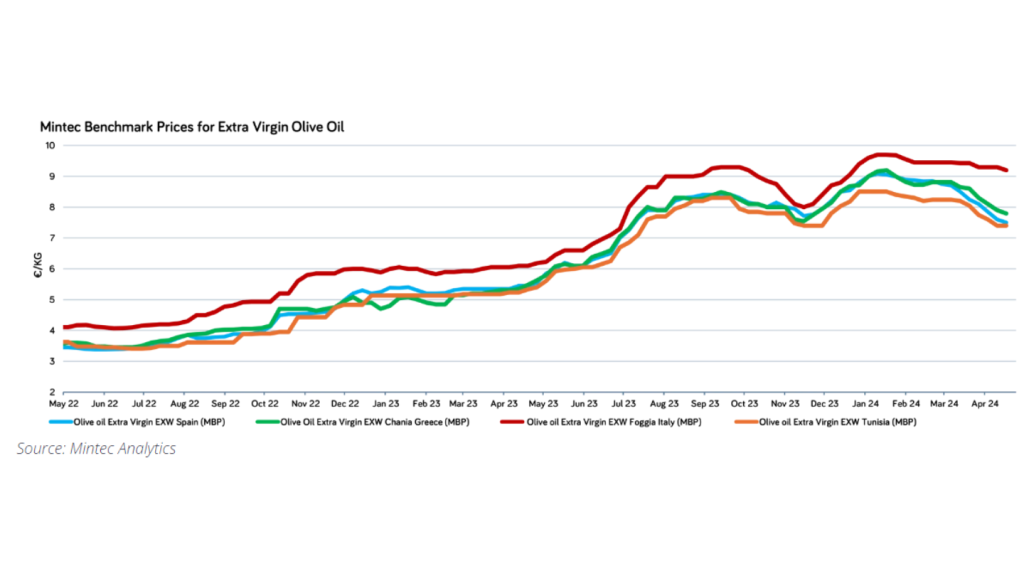

In the IOC’s weekly pricing statistics for May, refined olive oil prices in Jaén stood at €660 ($716) per 100kg, 37.2% higher than the same period in the previous crop year. Extra virgin olive oil was up 36.1% to €710 per 100kg.

Falling supplies mean rising prices

Spain’s Deoleo, the largest olive oil company in the world, posted a net loss of €34m ($37m) in its full-year results for 2023, noting an “exceptional and atypical market context, marked by high inflation and unfavourable olive oil harvest forecasts”.

However, the private-equity backed company recorded EBITDA of €30m after price rises. This figure was still down 30% on the previous year.

Ignacio Silva, chairman and CEO of Deoleo, said following the group’s results: “We have had an exceptionally challenging and highly volatile year, with two consecutive years of very poor harvests, both in terms of quality and quantity, and prices at historic levels.”

He added: “Although we expect the current year to continue to be challenging, we are confident that the current situation will normalise and we will see a strengthened sector in the medium term.”

Joseph R. Profaci, executive director of the North American Olive Oil Association (NAOOA), tells Just Food that “many companies are hopeful” that prices will ease back down soon.

“The last thing they want is to see consumers start switching back to other cooking oils and fats, which has happened in Europe to some extent where average prices increased almost 50% over the past year.”

The European Commission’s short-term outlook for EU agricultural markets agreed with Profaci, saying that EU consumption fell 20% in the last marketing year, and the association expects “some additional reduction”.

The body estimates that EU consumption could reach a historical low of below 1.2 million tonnes this year.

Starting stocks for the season were 406,000 tonnes, and ending stocks are expected to drop to 365,000 tonnes due to revived imports from traditional trading partners, such as Turkey and Tunisia, and Southern Hemisphere producers, including Argentina and Chile.

“While the level of beginning stocks might look comfortable, it is mainly due to a reduced demand, both in the EU and globally,” the Commission wrote.

Why is olive oil production down?

As the biggest producer of olive oil in the world, Spain’s supply is exceptionally important to the global industry.

However, following an unseasonably warm spell in the Mediterranean region in the winter of 2022/23, the olive trees did not have a chilling period to be able to flower and therefore create fruit for the following growing season, according to Aaron Hanson, senior economist at in the agribusiness division of GlobalData, Just Food‘s parent company .

He says two winters ago the chilling requirement was not met for a substantial share of olive trees “which meant Spain’s production the following summer – last summer – was expected to fall significantly”.

This was then followed by two years of the lowest rainfall that Spain has seen in 30 years.

Profaci claims the surging prices of olive oil in the last 18 months were the result of a “perfect storm”.

He said: “The worldwide general inflation on all goods and services began impacting the olive oil sector as early as 2021, in particular in terms of freight and material costs. Then, to compound matters, for the past two years running, drought and high temperatures in olive growing regions, but especially in Spain which normally produces close to half the world’s olive oil, severely impacted production, causing tight supplies and a spike in prices.

“On top of all that, consumers continue to become more aware of olive oil’s advantages over other cooking oils in terms of taste, health and sustainability. While this is of course a good thing for the industry, the continued growth in demand also contributed to the increase in prices.”

Greece, another major olive oil-producing nation, has also faced significant challenges with heat and the olive fly, a species of fruit fly whose larvae feed on the fruit of olive trees.

According to agri-food research, industry insiders predict olive oil production of “around 120,000 metric tonnes in 2023/24, a significant decrease from the previous year’s production of approximately 340,000 metric tonnes” in Greece.

Meanwhile, Turkey, a key supplier to the EU, is expected to produce “as little as 180,000 metric tonnes of olive oil, compared to approximately 410,000 metric tonnes in the prior season”, the research reported.

What are the effects?

Olivier Fevre, another analyst at GlobalData, recently noted that the olive oil shortage is a “double-edged sword for olive oil companies”.

He wrote in a briefing: “Higher prices mean bigger profit margins in the short term, with value of sales, in the UK, forecasted to experience a 4.3% three-year CAGR between 2023 and 2026. However, it is also likely to lead to stagnant sales in terms of volume as consumers cut back. To effectively navigate this landscape, olive oil companies may need to implement strategic initiatives such as diversifying their product offerings to include lower-priced options.”

The analyst also noted that “criminal organisations” are seeing an opportunity to resell the “liquid gold” on a black market.

He wrote: “Combatting the criminal activity is also important, where brands can invest in counterfeit detection technology such as blockchain and AI to create a trackable record of olive oil from farm to shelf.”

Last year, Profaci spoke to Just Food regarding the problems of bad actors in the North American olive oil scene but reaffirms now that the NAOOA has “not seen signs of any significant market disruption”.

Consumer demand nevertheless remains at some of the highest levels that the industry has ever seen, with a surge in a health and wellness trend for consumers who are acknowledging the benefits of olive oil. Similarly, the rise of the Mediterranean diet has helped spur demand.

However, the European Commission reported that Spain, Italy, Portugal and Greece, where olive oil is a staple, are expected to experience declines in consumption. The commission estimates consumption will fall below 900,000 tonnes, marking a 19.9% decrease compared with the average of the past five years.

Olive oil consumption per capita in the EU is also expected to decrease in the 2023/24 season, falling to 2.6 kilograms, a 19.2% drop compared to the five-year average.

Eurostat notes that olive oil prices were on average 50% higher in January 2024 than they were a year before. The increase in Italy, for example, was reported at 45%. As a result, the IOC is predicting that Italian olive oil consumption this year will drop 13%.

Meanwhile, demand in the US remains relatively stable, according to the NAOOA. Dusan Kaljevic, CEO of olive oil giant Filippo Berio’s US division, said: “The US market has been relatively resistant to pricing pressure and has moderated its demand of olive oil only slightly, which we believe speaks to the market’s appreciation of the health and culinary benefits of high-quality extra virgin olive oil.”

Will the tide turn?

The NAOOA recently revealed that the recent Holy Week in Spain, which takes place just before Easter, saw a “small miracle” where it rained the entire week.

The group said: “The years-long drought decimated output of the world’s largest olive-producing country and threatened drinking water supplies. The reservoir in Cordoba in Andalusia, for instance, was at a perilous 14% capacity on March 25. After a week of heavy rains, it has exceeded 70%.

“The rain and replenishment of reservoirs is good news and portends a potential return to pre-drought levels of production in Spain. This is helping pump the brakes on rising global olive prices, which were being fuelled in part by fears about the 2024/25 harvest. Not all areas of Spain received equal relief, but the rain in Andalusia (the region responsible for approximately half of Spanish olive production) bodes well for next year’s crop – barring other risk factors that could impact fruit development in the coming weeks.”

Profaci adds that this rain “was a positive sign” that the harvest may see a resurgence in the back half of the year.

He also notes that the olive oil industry saw a similarly dire two-year period of drought around 30 years ago which restabilised shortly afterwards. He is “optimistic history will repeat itself” but also does not “have a crystal ball”.

“If I have learned anything about this industry in my thirty-plus years experience, it’s that you can always expect the unexpected.”

The olive oil industry is facing a period of serious uncertainty as extreme weather, global cost pressures and inflation all weigh in on shortened supply.

Prices look set to continue a fluctuating pattern despite some short-term forecasts suggesting stability, as consumers will begin looking at alternativesl. Meanwhile, diminishing stocks could lead to a further rapid increase in prices from some companies as they run out of leftover supply.